House rental tax in Nepal is a direct tax imposed on income earned from renting out property. Whether you own a residential house, commercial space, or land and lease it to tenants, the income you receive is taxable under Nepal’s income tax laws. The Inland Revenue Department (IRD) of Nepal administers and collects this tax.

Understanding rental income tax is essential for both property owners and tenants, particularly businesses that pay rent and must comply with Tax Deducted at Source (TDS) obligations.

What is House Rental Tax in Nepal?

House rental tax in Nepal refers to the tax levied on income derived from renting out immovable property such as houses, apartments, commercial buildings, land, or any other structure. This income falls under “Income from Investment” as defined under the Income Tax Act, 2058 (2002) of Nepal.

Any individual, company, or entity that earns rental income from a property located in Nepal is required to declare that income and pay the applicable tax to the government. The Inland Revenue Department (IRD) of Nepal, operating under the Ministry of Finance, is the designated authority for collecting and managing rental income tax across the country.

Rental tax applies regardless of whether the tenant is an individual, a private company, a public enterprise, or a foreign organization. The obligation to pay tax on rental income rests with the property owner. However, when the tenant is a business entity, the responsibility to deduct TDS at the time of payment also falls on the tenant.

Legal Framework Governing Rental Income Tax in Nepal

The primary legislation governing house rental tax in Nepal is the Income Tax Act, 2058 (2002). Several sections of this Act directly deal with rental income.

| Legal Provision | Description |

|---|---|

| Income Tax Act, 2058 | Primary law governing all income taxes including rental income |

| Section 9 | Defines assessable income, which includes rental income under investment income |

| Section 88 | TDS obligations on rent payments made by businesses |

| Section 95A | Withholding tax on rent paid to non-residents |

| Finance Act (Annual) | Revises tax rates, slabs, and thresholds every fiscal year |

| Schedule 1 | Specifies tax rates applicable to natural persons and entities |

The Finance Act passed by the Parliament of Nepal every year (in the month of Ashad/June-July) revises tax slabs, thresholds, and rates. Taxpayers must always check the most recent Finance Act to confirm applicable tax rates for the current fiscal year.

The IRD Nepal publishes official guidelines at https://ird.gov.np.

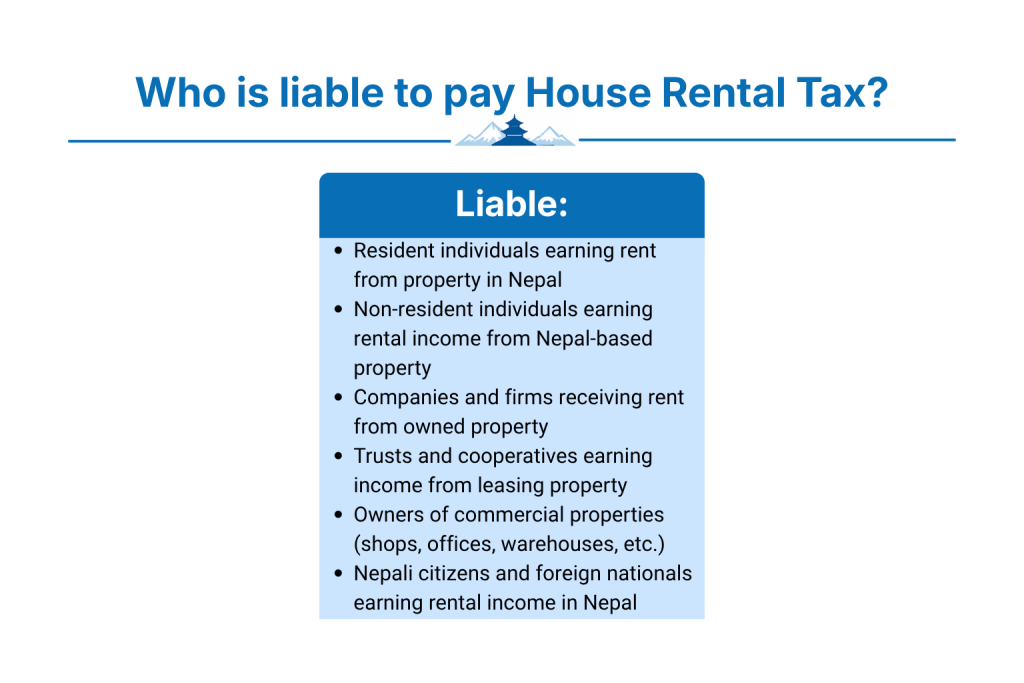

Who is Liable to Pay House Rental Tax in Nepal?

Under the Income Tax Act, 2058, the following persons are liable to pay rental income tax:

- Resident individuals who own property in Nepal and receive rent from tenants

- Non-resident individuals who own property in Nepal and lease it to others

- Registered companies and firms that earn rental income from property they own

- Trusts and cooperatives that receive income from leasing immovable assets

- Landlords of commercial properties such as office buildings, warehouses, and shops

Both Nepali citizens and foreign nationals owning property inside Nepal must pay tax on rental income earned from that property. If a foreign national earns rental income from property located in Nepal, the income is still subject to Nepal’s tax laws as it is a Nepal-source income.

House Rental Tax Rates in Nepal

Rental income in Nepal is taxed as part of the total assessable income of an individual or entity. For resident natural persons, rental income is added to their total income and taxed according to the progressive income tax slabs specified in the Finance Act.

Tax Slabs for Resident Individuals (FY 2080/81)

| Taxable Income (Annual) | Tax Rate (Single) | Tax Rate (Married/Couple) |

|---|---|---|

| Up to Rs. 5,00,000 | 1% | 1% (up to Rs. 6,00,000) |

| Rs. 5,00,001 to Rs. 7,00,000 | 10% | 10% |

| Rs. 7,00,001 to Rs. 20,00,000 | 20% | 20% |

| Rs. 20,00,001 to Rs. 50,00,000 | 30% | 30% |

| Above Rs. 50,00,000 | 36% | 36% |

These rates apply to the total income, which includes rental income combined with salary, business income, and other investment income. If rental income is the sole or primary income source, it is taxed within these slabs after applicable deductions.

For registered entities and companies, rental income is taxed as part of business income at the corporate tax rate, which is generally 25% for most entities, though rates vary depending on the nature of the business.

TDS on House Rent in Nepal (Section 88 of Income Tax Act, 2058)

Tax Deducted at Source (TDS) on rent is one of the most frequently discussed aspects of rental tax in Nepal. Under Section 88 of the Income Tax Act, 2058, a resident person who makes a rent payment in the course of conducting a business must withhold tax at the rate of 10% at the time of payment.

Key Points on TDS on Rent

- The tenant (payer of rent) is responsible for deducting 10% TDS before remitting rent to the landlord

- This obligation applies when the tenant is a registered business, company, organization, government body, or institution

- The deducted TDS must be deposited with the IRD through the Inland Revenue Office within 25 days of the end of the month in which the deduction was made

- The tenant must also issue a TDS certificate to the landlord, which the landlord uses when filing their annual income tax return

- The TDS deducted is treated as an advance tax payment for the landlord and is adjusted against their final tax liability

If an individual tenant (not operating a business) pays rent to a landlord, no TDS obligation exists. In such cases, the landlord must independently declare and pay the tax on rental income when filing their annual tax return.

Deductions Allowed on Rental Income in Nepal

Nepal’s Income Tax Act, 2058 allows landlords to claim certain deductions before calculating their net taxable rental income. These deductions reduce the gross rental income to arrive at the taxable amount.

Allowable Deductions for Rental Income

- Repair and maintenance expenses: Actual documented repair costs incurred on the rented property during the fiscal year

- Depreciation: Depreciation on building and fixtures as allowed under the Income Tax Act schedules

- Interest on loans: If a loan was taken to purchase or construct the rental property, interest paid on that loan is deductible

- Property tax (Malpot): Local property taxes paid to the municipality or rural municipality are deductible as business expenses for entities

- Insurance premiums: Premiums paid for property insurance covering the rented building

Landlords who are individual taxpayers must retain all bills, receipts, and documentation related to these deductions. The IRD may request supporting documents during tax assessment or audit.

How to File Rental Income Tax in Nepal

Filing rental income tax in Nepal follows a structured process. Both individuals and entities must comply with the annual self-assessment tax filing requirement.

Step-by-Step Process for Filing Rental Income Tax

- Obtain a Permanent Account Number (PAN) from the Inland Revenue Office if not already registered

- Calculate gross rental income received during the fiscal year (Shrawan to Ashad, i.e., mid-July to mid-July)

- Deduct allowable expenses (repair, depreciation, interest, insurance) to arrive at net taxable rental income

- Add net rental income to other income sources to compute total assessable income

- Apply the applicable tax slab to calculate gross tax liability

- Subtract TDS already deducted by tenants (if applicable) from the total tax liability

- Pay any remaining tax through advance tax payments or final settlement

- File the annual income tax return online through the IRD e-filing portal at https://ird.gov.np or in person at the relevant Inland Revenue Office

- Submit supporting documents including TDS certificates, rent agreements, and expense receipts

Documents Required for Filing Rental Income Tax

- PAN card copy

- Rent agreement (Bhaada Sahamati Patra)

- TDS certificates from tenants (if applicable)

- Bank statements showing rent receipts

- Receipts for repair and maintenance expenses

- Loan statements (if claiming interest deduction)

- Property ownership documents (Lalpurja)

The deadline for filing the annual income tax return for individuals is generally Poush end (approximately January) of the following fiscal year, which gives taxpayers approximately six months from the fiscal year end to file their returns.

Penalties for Non-Compliance with Rental Tax in Nepal

The Income Tax Act, 2058 prescribes penalties for failure to comply with rental tax obligations. The IRD enforces these penalties during tax assessments and audits.

- Failure to file tax return: A penalty of Rs. 100 per day for each day the return is overdue, subject to a maximum as prescribed by the Act

- Underpayment or non-payment of tax: Interest at the rate of 15% per annum on the unpaid tax amount from the due date

- Failure to deduct TDS: Tenants who fail to deduct TDS on rent payments are treated as if the unpaid TDS is still owed to the government, and they may be required to pay the full amount plus penalties

- Tax evasion: Serious cases of deliberate tax evasion can attract prosecution under the Income Tax Act, leading to fines and possible imprisonment

The IRD conducts periodic audits of rental income declarations, particularly in urban areas such as Kathmandu, Lalitpur, and Pokhara, where rental markets are active. Landlords who fail to declare rental income face back-tax assessments plus penalties and interest.

Rental Tax for Non-Resident Landlords

Foreign nationals or non-resident Nepali citizens who earn rental income from property located in Nepal must pay tax on that income under Section 95A of the Income Tax Act, 2058. The TDS rate applicable to rent payments made to non-residents is 15%, which is higher than the standard 10% TDS applicable for resident landlords. The tenant or the person making the payment is responsible for deducting this higher rate and depositing it with the IRD.

Conclusion

House rental tax in Nepal is governed by the Income Tax Act, 2058 and administered by the Inland Revenue Department. Property owners who earn rental income must obtain a PAN, calculate their net rental income after allowable deductions, and file an annual income tax return. Tenants who are registered businesses must deduct 10% TDS on rent payments and deposit it with the IRD within the prescribed deadline. Non-compliance attracts interest, penalties, and possible prosecution. Landlords and tenants should regularly consult the IRD website and the latest Finance Act to stay updated on current tax rates and filing requirements.

FAQs

1. Is rental income from a single room taxable in Nepal?

Yes. Any rental income, regardless of the amount, is technically taxable in Nepal under the Income Tax Act, 2058. However, if total annual income including rent falls below the minimum taxable threshold, the effective tax rate is 1% on the first Rs. 5,00,000.

2. What is the TDS rate on rent in Nepal?

Under Section 88 of the Income Tax Act, 2058, the TDS rate on rent paid by a business or organization to a resident landlord is 10%. For non-resident landlords, the rate is 15% under Section 95A.

3. Does a landlord need to register with the IRD to pay rental tax?

Yes. A landlord earning rental income must obtain a Permanent Account Number (PAN) from the Inland Revenue Office. PAN registration is mandatory for all persons with taxable income in Nepal, including rental income earners.

4. Can a landlord deduct repair costs from rental income before paying tax?

Yes. Actual repair and maintenance expenses incurred on the rented property during the fiscal year are deductible from gross rental income. The landlord must maintain proper bills and receipts to support these deductions during tax filing or audit.

5. What happens if a tenant does not deduct TDS on rent?

If the tenant, being a registered business, fails to deduct TDS on rent, the IRD treats the unpaid TDS as a liability of the tenant. The tenant may be required to pay the full TDS amount, plus interest at 15% per annum and applicable penalties under the Income Tax Act, 2058.

6. Where can a landlord file their rental income tax return in Nepal?

Landlords can file their annual income tax return online through the IRD e-filing portal at https://ird.gov.np or in person at the nearest Inland Revenue Office. The filing deadline is generally the end of Poush (mid-January) of the following fiscal year.