The dividend distribution process in Nepal follows a structured legal framework governed by the Companies Act 2063 (2006), the Securities Act 2063 (2007), and directives issued by the Securities Board of Nepal (SEBON) and Nepal Rastra Bank (NRB). Understanding the dividend distribution process in Nepal helps shareholders, company directors, and investors make informed decisions about corporate earnings, profit sharing, and investment returns.

What Is Dividend Distribution in Nepal?

Dividend distribution in Nepal refers to the process by which a company distributes a portion of its net profit to its shareholders. The distribution can be in the form of cash dividend, stock dividend (bonus shares), or both. Companies listed on the Nepal Stock Exchange (NEPSE) must follow specific regulatory procedures before distributing dividends.

Dividends are typically declared from the company’s retained earnings or net profit after tax. Under Section 182 of the Companies Act 2063, a company may distribute dividends only from distributable profits.

What Are the Types of Dividends in Nepal?

Nepal recognizes the following types of dividends:

| Type of Dividend | Description | Tax Treatment |

|---|---|---|

| Cash Dividend | Company pays dividend in cash to shareholders | 5% withholding tax for residents; 15% for non-residents |

| Stock Dividend (Bonus Shares) | Company issues additional shares instead of cash | 5% withholding tax applicable |

| Interim Dividend | Dividend declared before the end of the fiscal year | Subject to same tax rules |

| Final Dividend | Declared after Annual General Meeting (AGM) approval | Subject to same tax rules |

Under the Income Tax Act 2058 (2002), dividend income is subject to a final withholding tax of 5% for resident individuals and 15% for non-resident shareholders.

What Laws Govern Dividend Distribution in Nepal?

The dividend distribution process in Nepal is governed by several laws and regulatory bodies:

- Companies Act 2063 (2006) – Sections 180–184 deal with dividend distribution rules

- Securities Act 2063 (2007) – Governs listed companies and SEBON directives

- Income Tax Act 2058 (2002) – Defines tax obligations on dividend income

- Nepal Rastra Bank Act 2058 (2002) – Governs dividend distribution of banks and financial institutions (BFIs)

- Bank and Financial Institution Act (BAFIA) 2073 (2017) – Restricts dividend distribution unless certain capital adequacy ratios are met

- SEBON Directives – Provide procedural guidelines for listed companies

Companies that fail to comply with these provisions face penalties under the respective Acts.

What Is the Dividend Distribution Process in Nepal Step by Step?

The dividend distribution process in Nepal involves multiple steps from board approval to final payment. Here is the complete process:

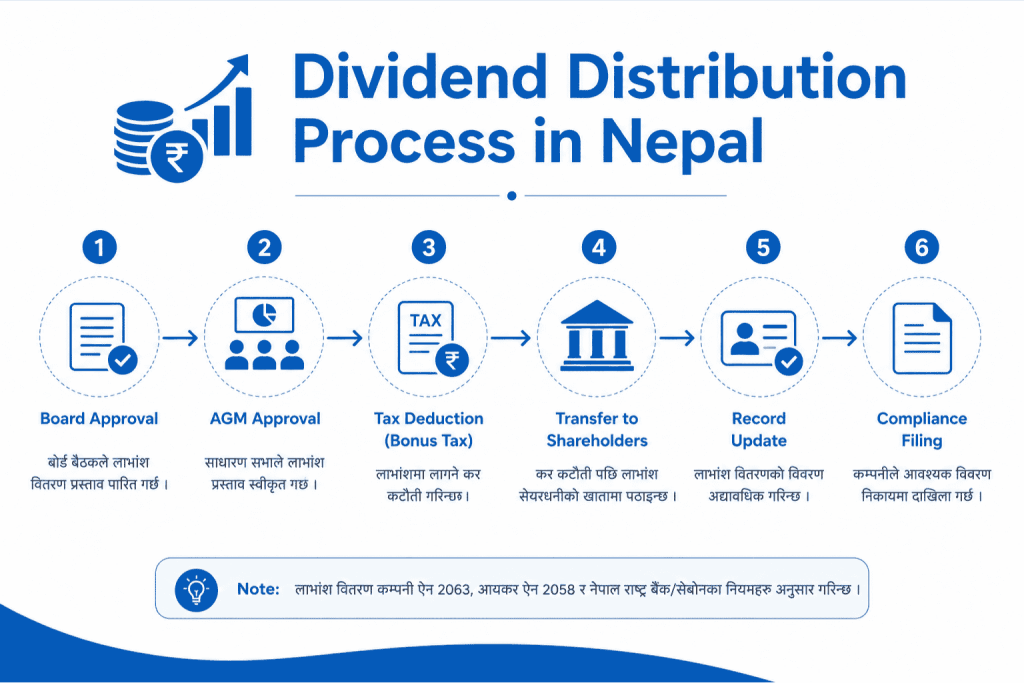

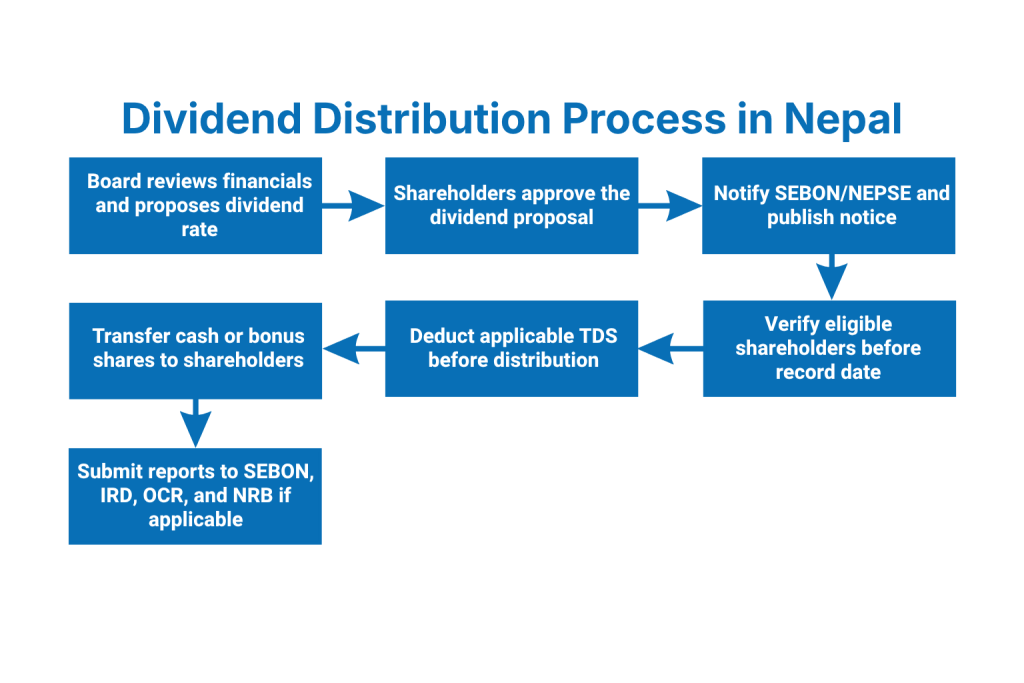

Step 1: Board of Directors Meeting

- The Board of Directors (BOD) reviews the company’s financial statements

- The board proposes the dividend rate (e.g., 10% cash dividend or 15% stock dividend)

- The BOD passes a formal resolution recommending the dividend

Step 2: Annual General Meeting (AGM) Approval

- The company convenes an Annual General Meeting (AGM) as per Section 76 of the Companies Act 2063

- Shareholders vote to approve the proposed dividend

- The approved dividend rate is formally announced

Step 3: Dividend Announcement and SEBON/NEPSE Filing

- Listed companies notify SEBON and Nepal Stock Exchange (NEPSE) about the dividend decision

- The company publishes a public notice in a national newspaper

- NEPSE sets the Book Closure Date and Ex-Dividend Date

Step 4: Book Closure and Record Date

- The company closes its share register for a specific period

- Only shareholders registered before the Record Date are eligible for the dividend

- CDSC (CDS and Clearing Limited) verifies the shareholder register

Step 5: Tax Deduction at Source (TDS)

- The company deducts 5% TDS (Tax Deducted at Source) on cash dividends for resident shareholders

- For non-resident shareholders, 15% TDS applies under the Income Tax Act 2058

- The deducted tax is deposited with the Inland Revenue Department (IRD)

Step 6: Dividend Payment

- Cash dividends are transferred directly to shareholders’ bank accounts linked with their Demat accounts

- Stock dividends (bonus shares) are credited to shareholders’ CDS (Central Depository System) accounts

- The process must be completed within 45 days of AGM as per SEBON directives

Step 7: Reporting to Regulatory Bodies

- The company submits dividend distribution reports to SEBON, IRD, and the Office of the Company Registrar (OCR)

- BFIs also report to Nepal Rastra Bank (NRB)

What Documents Are Required for Dividend Distribution?

The company must prepare and submit the following documents:

- Board Resolution approving dividend recommendation

- AGM Minutes confirming shareholder approval

- Audited Financial Statements for the relevant fiscal year

- Shareholder Register as maintained by CDSC

- TDS Deposit Challan submitted to IRD

- Dividend Distribution Report filed with SEBON and OCR

- Public Notice published in a national newspaper (for listed companies)

- Bank Authorization Letter for direct transfer to shareholders’ accounts

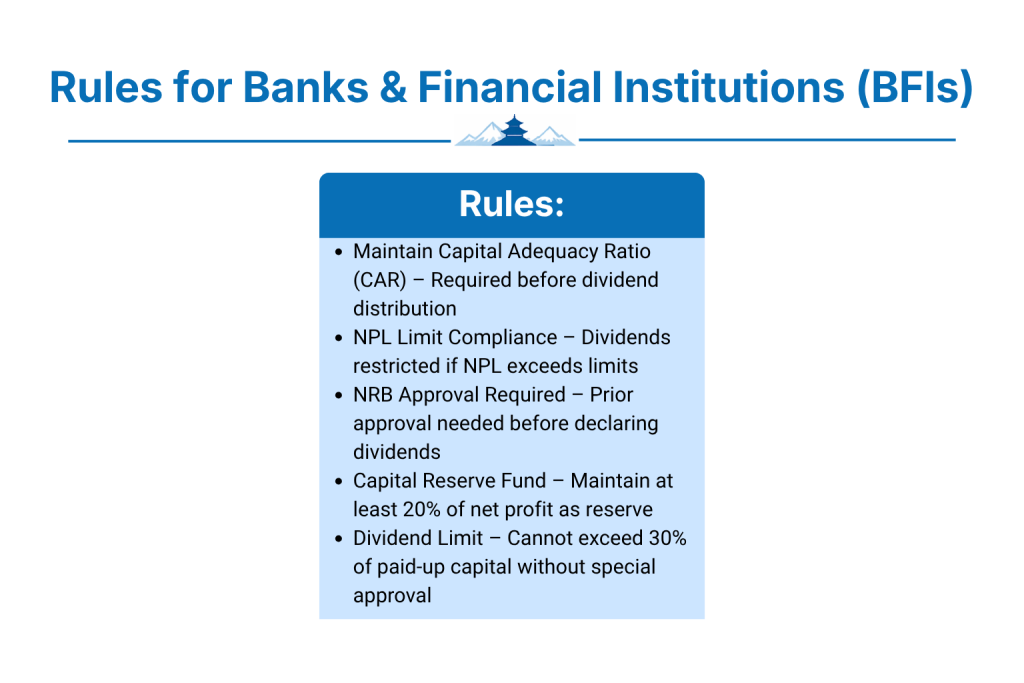

What Are the Rules for Banks and Financial Institutions (BFIs)?

Nepal Rastra Bank has strict rules for dividend distribution by banks and financial institutions. Under BAFIA 2073 and NRB directives:

- BFIs must maintain the Capital Adequacy Ratio (CAR) before distributing dividends

- BFIs cannot distribute dividends if they have non-performing loans (NPL) exceeding prescribed limits

- Prior approval from NRB is required before declaring dividends

- BFIs must maintain a Capital Reserve Fund equal to at least 20% of net profit before distributing dividends

- Dividends cannot exceed 30% of the paid-up capital unless NRB gives special permission

For more information on NRB regulations, visit the official NRB website: https://www.nrb.org.np

What Are the Tax Implications of Dividend Distribution in Nepal?

Dividend taxation in Nepal is clear and straightforward under the Income Tax Act 2058:

Shareholder TypeTDS RateRemarksResident Individual5%Final withholding taxNon-Resident Individual15%As per Section 88Resident Company5%Inter-corporate dividendNon-Resident Company15%Subject to DTAA

- Nepal has Double Taxation Avoidance Agreements (DTAA) with countries including India, China, Mauritius, and others

- Under DTAA provisions, non-resident shareholders may pay reduced tax rates

- Companies must file TDS returns with the Inland Revenue Department within the prescribed time

For tax-related information, visit the IRD official portal: https://www.ird.gov.np

What Are the Restrictions on Dividend Distribution in Nepal?

Under Section 184 of the Companies Act 2063, companies face certain restrictions on dividend distribution:

- A company cannot declare dividends if it has accumulated losses

- A company cannot pay dividends out of capital or from funds required for capital maintenance

- Dividends cannot be declared if the company is unable to pay its debts as they fall due

- Companies must first transfer at least 10% of net profit to a General Reserve Fund before declaring dividends

- Cooperative companies must also comply with the Cooperative Act 2074 (2017) before distributing profits

What Is the Role of CDSC in Dividend Distribution?

CDS and Clearing Limited (CDSC) plays a central role in the dividend distribution process in Nepal:

- CDSC maintains the Central Depository System for all securities in Nepal

- It provides the verified shareholder list to companies for dividend processing

- For stock dividends, CDSC directly credits bonus shares to the Demat accounts of eligible shareholders

- For cash dividends, CDSC verifies bank account details linked to Demat accounts for direct credit

Visit the official CDSC website: https://www.cdsc.com.np

What Happens If a Company Fails to Distribute Dividends?

If a company declares a dividend but fails to distribute it within the prescribed period:

- The company faces penalties under Section 183 of the Companies Act 2063

- SEBON can take action against listed companies for non-compliance

- Shareholders have the right to file a complaint with the Office of the Company Registrar (OCR)

- In the case of BFIs, NRB can suspend the management of the institution

- Unclaimed dividends remain a liability on the company’s balance sheet

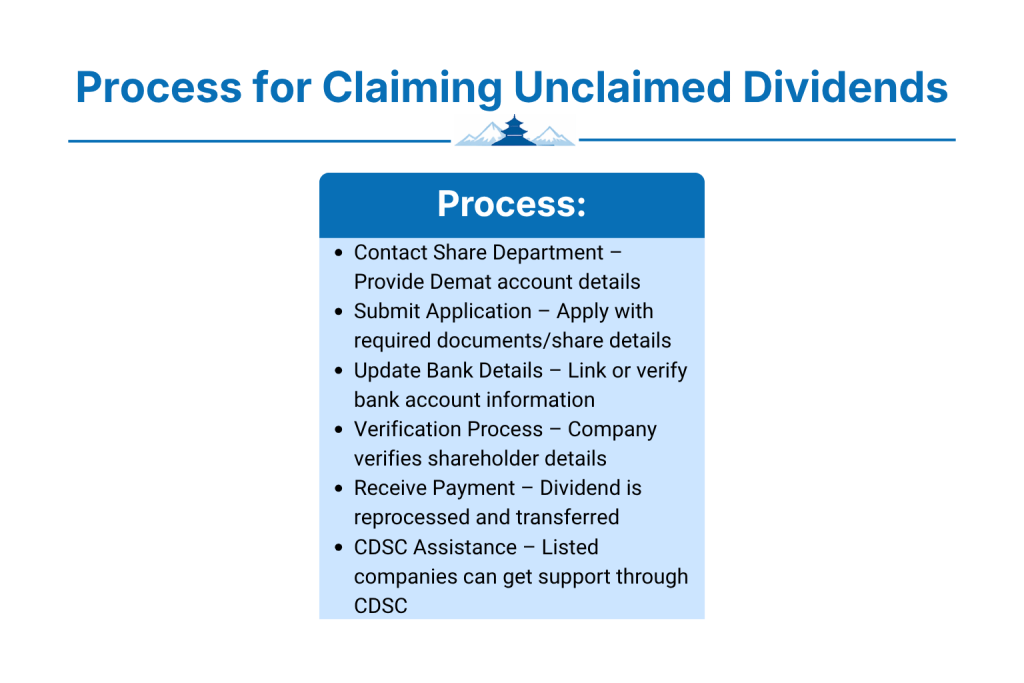

What Is the Process for Claiming Unclaimed Dividends in Nepal?

Shareholders who have not received their declared dividends can claim them through the following process:

- Contact the company’s Share Department with Demat account details

- Submit a written application along with share certificate copy (if applicable)

- Provide updated bank account details linked with the Demat account

- The company reprocesses the payment after verification

- For listed companies, CDSC also assists in resolving unclaimed dividend issues

Conclusion

The dividend distribution process in Nepal follows a well-defined legal structure under the Companies Act 2063, Securities Act 2063, Income Tax Act 2058, BAFIA 2073, and various SEBON and NRB directives. The process involves board approval, AGM authorization, regulatory filings, book closure, TDS deduction, and final payment through the CDSC system. Shareholders must ensure their Demat accounts and bank account details are updated to receive dividends without delays. Companies must strictly follow the prescribed timelines and regulatory requirements to avoid penalties and ensure smooth dividend distribution to all eligible shareholders.

FAQs

1. What is the time limit for dividend payment after AGM in Nepal?

Under SEBON directives, listed companies must complete dividend payment within 45 days of the Annual General Meeting (AGM) approval. Failure to comply results in regulatory action by SEBON and the OCR.

2. Is dividend income taxable in Nepal?

Yes, dividend income is taxable in Nepal. A 5% final withholding tax applies to resident shareholders, while 15% TDS applies to non-resident shareholders under the Income Tax Act 2058.

3. Can a company distribute dividends without AGM approval in Nepal?

No. Under the Companies Act 2063, dividends must be approved by shareholders at the Annual General Meeting (AGM). Only interim dividends can be declared by the board without AGM approval in certain cases.

4. What is a bonus share dividend in Nepal?

A bonus share (stock dividend) is when a company issues additional shares to existing shareholders instead of cash. These shares are credited directly to shareholders’ Demat accounts through the CDSC system.

5. Can banks in Nepal distribute dividends freely?

No. Banks and financial institutions must obtain prior approval from Nepal Rastra Bank (NRB) and must meet capital adequacy ratios under BAFIA 2073 before distributing any form of dividend.

6. Where can shareholders check dividend announcements in Nepal?

Shareholders can check dividend announcements on the official NEPSE website at https://www.nepalstock.com.np, the SEBON website at https://www.sebon.gov.np, or the company’s official notice published in national newspapers.