The Annual General Meeting process in Nepal is a mandatory corporate governance requirement for all registered companies operating under Nepali law. The AGM serves as the primary platform where shareholders, directors, and auditors come together to review the company’s financial performance, approve key decisions, and fulfill statutory obligations.

Understanding the AGM process in Nepal is essential for company directors, shareholders, company secretaries, legal professionals, and business owners alike.

What Is an Annual General Meeting (AGM) in Nepal?

An Annual General Meeting (AGM) is a formal yearly assembly of a company’s shareholders and board of directors. In Nepal, the AGM is governed primarily by the Companies Act, 2063 (2006) and the Securities Act, 2063 (2007) for listed companies. The Office of the Company Registrar (OCR) Nepal oversees compliance related to AGM requirements.

The AGM in Nepal allows the company to:

- Present and approve annual financial statements

- Appoint or reappoint auditors

- Declare dividends

- Elect or reelect directors

- Discuss and approve major company decisions

What Is the Legal Framework Governing AGM in Nepal?

The Companies Act, 2063 (2006) is the primary legislation governing AGMs in Nepal. The relevant provisions are detailed under Chapter 7 (Sections 68–86) of the Act. Additional regulations apply to publicly listed companies under the Securities Act, 2063 and directives issued by the Securities Board of Nepal (SEBON).

Key Legal Provisions:

| Legal Provision | Description |

|---|---|

| Section 68, Companies Act 2063 | Mandates holding of AGM every fiscal year |

| Section 69, Companies Act 2063 | Specifies the time frame within which AGM must be held |

| Section 71, Companies Act 2063 | Deals with AGM notice requirements |

| Section 76, Companies Act 2063 | Defines quorum requirements for AGM |

| Section 79, Companies Act 2063 | Governs voting procedures at AGM |

| Securities Act, 2063 | Additional AGM requirements for listed companies |

You can access the full text of the Companies Act, 2063 at the Office of Company Registrar Nepal and SEBON directives at SEBON Nepal.

Who Is Required to Hold an AGM in Nepal?

Under Section 68 of the Companies Act, 2063, the following types of companies are required to hold an AGM:

- Private Limited Companies (Pvt. Ltd.) registered in Nepal

- Public Limited Companies (Ltd.) registered in Nepal

- Listed Public Companies regulated under SEBON

- Non-Profit Companies registered under the Companies Act

Sole proprietorships and partnership firms are not required to hold a formal AGM under the Companies Act.

When Must an AGM Be Held in Nepal?

Section 69 of the Companies Act, 2063 specifies the time limits for holding an AGM:

- A company must hold its first AGM within 6 months of the end of its first fiscal year.

- Subsequent AGMs must be held within 6 months from the end of each fiscal year.

- In Nepal, the fiscal year ends on Ashadh End (mid-July) each year.

- Therefore, most companies must hold their AGM by Poush end (mid-January) of the following year.

For listed companies, SEBON directives often impose stricter timelines, sometimes requiring AGM completion within three months after the fiscal year ends.

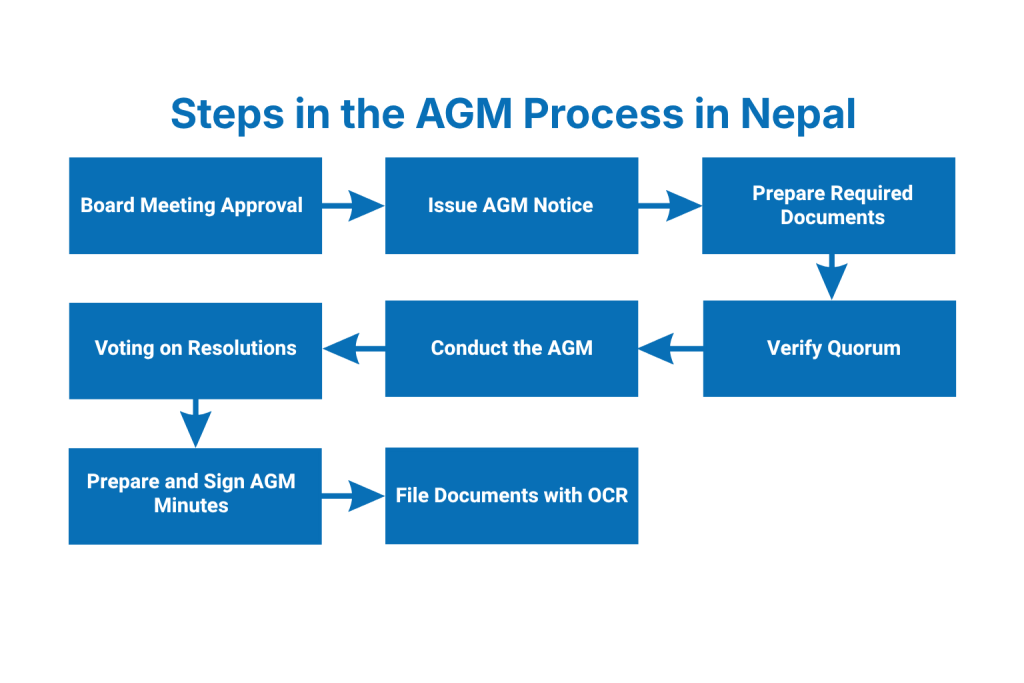

What Are the Steps in the AGM Process in Nepal?

The AGM process in Nepal follows a structured step-by-step approach from preparation to post-meeting compliance.

Step 1: Board Meeting to Approve AGM

The Board of Directors must first pass a resolution in a Board Meeting to:

- Fix the date, time, and venue of the AGM

- Approve the agenda of the meeting

- Approve the financial statements for the fiscal year

- Approve the auditor’s report

Step 2: Issuance of AGM Notice

Under Section 71 of the Companies Act, 2063, the company must issue a written notice to all shareholders at least 15 days before the AGM (21 days for public companies in practice for good governance).

The AGM notice must include:

- Date, time, and venue of the meeting

- Full agenda of the meeting

- Proxy form (if applicable)

- Annual financial statements (balance sheet, profit & loss)

- Auditor’s report

- Director’s report

For listed companies, SEBON requires the notice to be published in a national daily newspaper and also submitted to Nepal Stock Exchange (NEPSE) and SEBON in advance.

Step 3: Preparation of Required Documents

Before the AGM, the company must prepare and compile the following documents:

- Audited financial statements (Balance Sheet, Profit & Loss Account, Cash Flow Statement)

- Board of Directors’ report

- Auditor’s report

- Agenda paper

- Minutes book for the AGM

- Attendance sheet for shareholders

- Proxy forms submitted by shareholders

- Share register and updated shareholder list

Step 4: Verification of Quorum

Under Section 76 of the Companies Act, 2063, the AGM cannot proceed without a valid quorum.

- For private companies, a quorum requires at least 50% of the total shareholders to be present (either in person or by proxy).

- For public companies, the quorum is generally at least 5 shareholders or 5% of total shareholders, whichever is lower, subject to the company’s Articles of Association.

If quorum is not met within 30 minutes of the scheduled time, the meeting is adjourned to the next scheduled date.

Step 5: Conducting the AGM

The Chairperson of the Board typically chairs the AGM. The following items are addressed at the meeting:

- Reading and approval of minutes of the last AGM

- Presentation of the Directors’ Report

- Presentation of Audited Financial Statements

- Appointment or reappointment of auditors and fixing their remuneration

- Declaration of dividend (if any)

- Election or reelection of directors (if required)

- Discussion and approval of special resolutions (if any)

- Any other agenda item with prior notice

Step 6: Voting at the AGM

Under Section 79 of the Companies Act, 2063, voting at the AGM may be conducted by:

- Show of hands (for ordinary resolutions)

- Poll/ballot (for special resolutions or when demanded by shareholders)

- Proxy voting (by shareholders who cannot attend in person)

Ordinary resolutions require a simple majority (more than 50%) of votes. Special resolutions require a 75% majority of votes cast.

Step 7: Preparation and Signing of AGM Minutes

After the AGM concludes, the company secretary or designated officer must prepare the minutes of the AGM within a reasonable time. The minutes must:

- Record all decisions made at the meeting

- Include attendance details

- Be signed by the Chairperson of the meeting

- Be maintained in the company’s minute book

Step 8: Filing with the Office of Company Registrar (OCR)

After the AGM, the company must submit the following documents to the Office of Company Registrar Nepal:

- Copy of AGM minutes

- Audited financial statements

- Auditor’s report

- Directors’ report

- Any special resolutions passed

For listed companies, filings must also be made with SEBON and NEPSE.

What Are the Documents Required for AGM Filing in Nepal?

| Document | Required By |

|---|---|

| AGM Minutes (signed) | OCR Nepal |

| Audited Financial Statements | OCR / SEBON |

| Auditor’s Report | OCR / SEBON |

| Directors’ Report | OCR |

| List of Shareholders present | OCR |

| Special Resolution (if any) | OCR |

| Updated Director information | OCR |

| Dividend declaration details | SEBON (listed companies) |

What Happens If a Company Fails to Hold an AGM in Nepal?

Section 86 of the Companies Act, 2063 prescribes penalties for companies that fail to hold an AGM within the stipulated time frame.

- The Office of Company Registrar may impose a financial penalty on the company and its directors.

- Directors who willfully prevent or delay the AGM may face personal liability.

- The OCR has the authority to blacklist companies with persistent non-compliance.

- For listed companies, SEBON may suspend trading in the company’s shares until compliance is achieved.

- Shareholders may petition the court or OCR to compel the company to hold an AGM.

What Are Special Resolutions at an AGM in Nepal?

A special resolution at an AGM in Nepal requires a 75% majority vote of shareholders present and voting. Special resolutions are required for:

- Changing the company’s name

- Altering the Memorandum of Association (MOA) or Articles of Association (AOA)

- Increasing or reducing share capital

- Voluntarily dissolving the company

- Approving mergers or acquisitions

What Is the Role of the Auditor at an AGM in Nepal?

Under the Companies Act, 2063, a company’s auditor is appointed or reappointed at the AGM. The auditor:

- Presents the auditor’s report on the company’s financial statements

- Certifies whether the financial statements give a true and fair view of the company’s financial position

- Must be a registered auditor with the Institute of Chartered Accountants of Nepal (ICAN)

- Cannot serve as auditor for more than three consecutive years for the same company (as per ICAN guidelines)

Conclusion

The Annual General Meeting process in Nepal is a structured legal requirement governed by the Companies Act, 2063, SEBON regulations, and OCR guidelines. Companies must adhere strictly to the timelines, notice requirements, quorum provisions, voting procedures, and post-meeting filing obligations. Non-compliance exposes directors and companies to significant legal and financial consequences. Companies should maintain proper corporate governance practices and engage qualified company secretaries and chartered accountants to ensure full compliance with all AGM-related legal obligations in Nepal.

FAQs

1. What is the minimum notice period for an AGM in Nepal?

Under Section 71 of the Companies Act, 2063, the minimum notice period for an AGM in Nepal is 15 days for private companies. Public and listed companies generally follow a 21-day notice period as per good governance practices and SEBON directives.

2. Can a shareholder attend an AGM through a proxy in Nepal?

Yes. Under the Companies Act, 2063, shareholders who cannot attend the AGM in person may appoint a proxy representative to attend and vote on their behalf. The proxy form must be submitted to the company before the meeting.

3. What is the penalty for not holding an AGM in Nepal?

Under Section 86 of the Companies Act, 2063, the company and its responsible directors may face financial penalties imposed by the Office of Company Registrar (OCR). Listed companies may also face trading suspension by SEBON.

4. How soon must AGM minutes be filed with OCR in Nepal?

AGM minutes and related documents must be filed with the Office of Company Registrar (OCR) within 35 days of the AGM as per the Companies Act, 2063. Delays may attract penalties.

5. Is an AGM required for a single-member company in Nepal?

Under the Companies Act, 2063, single-member private companies are also required to comply with AGM requirements. However, the sole shareholder can fulfill the AGM formalities with simplified procedures as per OCR guidelines.

6. Can a listed company hold a virtual AGM in Nepal?

As of current legal provisions, virtual or online AGMs do not have explicit legal recognition under the Companies Act, 2063. Listed companies in Nepal are generally required to hold physical AGMs, though hybrid formats are being discussed by regulators at SEBON.

For further legal reference, visit the Office of Company Registrar Nepal, Securities Board of Nepal, and Nepal Stock Exchange.