In this article, we’ll explore the ins and outs of obtaining a banking license process in Nepal, from the application process to post-license requirements.

What is a Banking License in Nepal?

A banking license in Nepal is an official authorization granted by the country’s central regulatory authority, allowing an entity to operate as a bank within the nation. This license is essential for any organization wishing to engage in banking activities, such as accepting deposits, providing loans, and offering other financial services to the public.

The license serves as a seal of approval, indicating that the institution meets the necessary regulatory standards and has the financial capacity to operate safely and responsibly. It’s the first step in establishing a bank and is crucial for building trust with potential customers and partners in the Nepalese financial landscape.

Which Authority Issues Banking Licenses in Nepal?

In Nepal, the sole authority responsible for issuing banking licenses is Nepal Rastra Bank (NRB). As the central bank of Nepal, NRB plays a pivotal role in regulating and supervising the country’s financial sector.

NRB’s licensing department carefully evaluates each application to ensure that potential banks meet stringent criteria. This includes assessing the applicant’s financial stability, proposed business model, and ability to comply with relevant laws and regulations.

The central bank’s involvement doesn’t end with license issuance. NRB continues to monitor licensed banks to ensure ongoing compliance and financial health, safeguarding the interests of depositors and maintaining the stability of Nepal’s banking system.

What Laws Govern Banking Licensing in Nepal?

The banking licensing process in Nepal is governed by several key pieces of legislation:

- Banks and Financial Institutions Act (BAFIA)

- Nepal Rastra Bank Act

- Company Act

- Foreign Investment and Technology Transfer Act (if applicable)

- Anti-Money Laundering Act

- Foreign Exchange Regulation Act

- Electronic Transactions Act

These laws collectively establish the legal framework for banking operations in Nepal. They outline the requirements for obtaining and maintaining a banking license, set standards for corporate governance, and define the scope of permitted banking activities.

The BAFIA, in particular, is crucial as it provides detailed guidelines on the establishment, operation, and regulation of banks and financial institutions in Nepal. Aspiring bank owners must familiarize themselves with these laws to ensure full compliance throughout the licensing process and beyond.

What is the Process for Obtaining a Banking License?

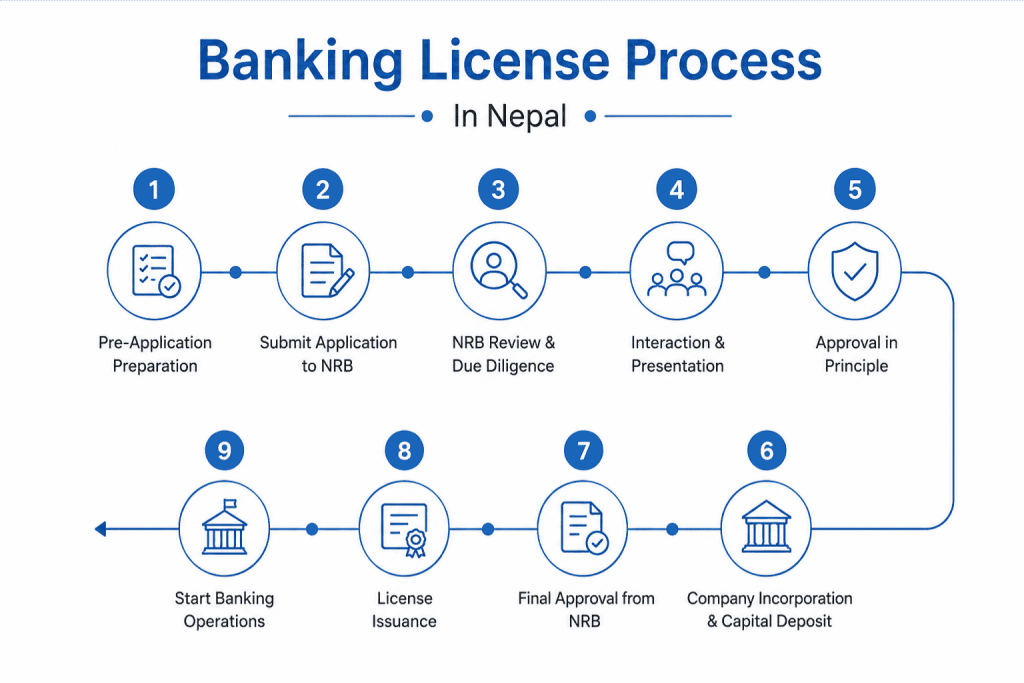

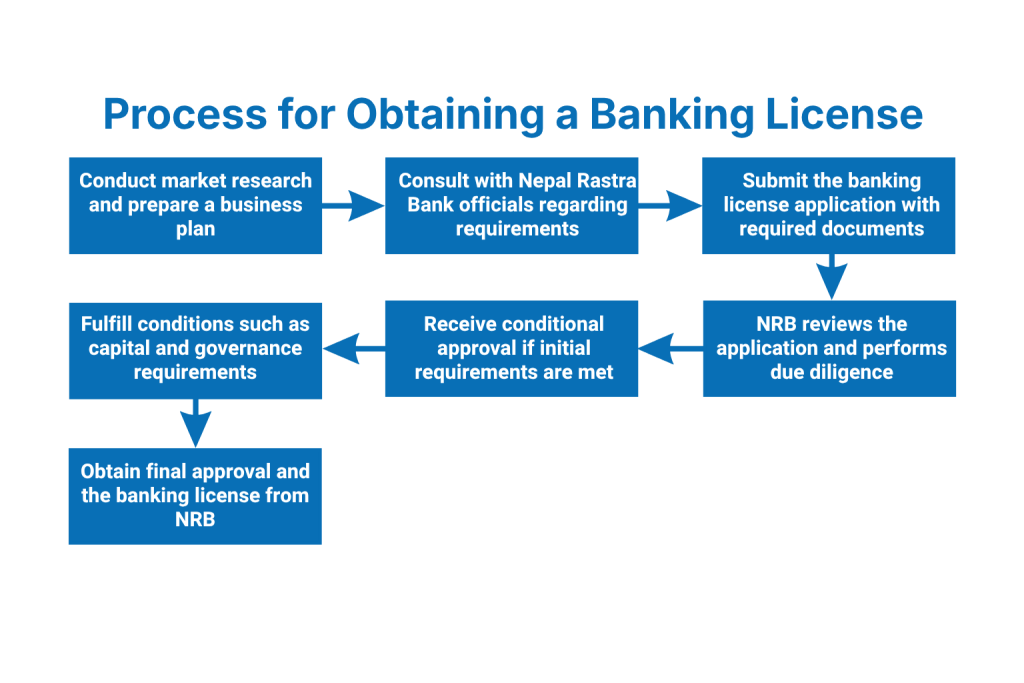

The process of obtaining a banking license in Nepal involves several steps and can be quite complex. Here’s a general overview of the key stages:

- Pre-application preparation: Research the market, develop a business plan, and gather necessary documents.

- Initial consultation: Meet with NRB officials to discuss your plans and understand specific requirements.

- Application submission: Submit a formal application to NRB along with all required documents and fees.

- Application review: NRB evaluates the application, conducting due diligence on the proposed bank’s financial capacity, ownership structure, and business model.

- Conditional approval: If the application meets initial criteria, NRB may grant conditional approval, outlining any additional requirements.

- Meeting conditions: Fulfill any conditions set by NRB, such as raising minimum capital or establishing governance structures.

- Final approval and licensing: Once all conditions are met, NRB issues the final banking license.

Throughout this process, clear communication with NRB is crucial. Be prepared for potential requests for additional information or clarification. The licensing process is designed to be thorough to ensure only qualified institutions enter the banking sector.

Read More:

Hospitality Company Registration in Nepal

Joint Venture Agreement Registration Process in Nepal

Educational Institution Affiliation Process in Nepal

It’s important to note that the exact steps may vary depending on the type of banking license sought and the specific circumstances of the applicant. Working with legal and financial experts familiar with Nepal’s banking sector can help navigate this complex process more efficiently.

What Documents are Required for the License Application?

Preparing a complete and accurate set of documents is crucial for a successful banking license application in Nepal. While the exact requirements may vary based on the type of license and the applicant’s circumstances, here are some key documents typically required:

- Detailed business plan

- Proof of minimum capital requirement

- Articles of Association and Memorandum of Association

- List of proposed shareholders and their background information

- Proposed organizational structure and management team profiles

- Financial projections for at least three years

- Risk management and compliance policies

- Anti-money laundering (AML) and know-your-customer (KYC) procedures

- IT infrastructure plans

- Details of proposed banking products and services

Each document plays a crucial role in demonstrating the applicant’s readiness to operate a bank. The business plan, for instance, should clearly outline the bank’s strategy, target market, and growth projections. Financial documents must show that the proposed bank meets capital requirements and has a sustainable business model.

NRB scrutinizes these documents closely, so it’s essential to ensure they are comprehensive, accurate, and professionally prepared. Consider engaging legal and financial experts to assist in document preparation to increase the chances of a successful application.

How Long Does the Banking License Process Take?

The duration of the banking license process in Nepal can vary significantly depending on various factors. On average, it can take anywhere from 6 months to 2 years from the initial application to the final license issuance.

Several factors can influence the timeline:

- Completeness of the application

- Complexity of the proposed bank’s structure

- NRB’s current workload and priorities

- Time taken to meet any additional requirements set by NRB

- Background checks on shareholders and key personnel

- Any changes in regulations during the application process

It’s important to note that this is not a linear process. There may be periods of waiting followed by intense activity as you respond to NRB’s queries or fulfill additional requirements. Patience and flexibility are key virtues during this process.

To potentially speed up the process, ensure your initial application is as complete and detailed as possible. Prompt responses to any NRB queries and quick fulfillment of any additional requirements can also help keep the process moving forward efficiently.

What are the Costs of Obtaining a Banking License?

Obtaining a banking license in Nepal involves several costs, both direct and indirect. While the exact amounts can vary, here’s an overview of the main expenses to consider:

- Application fee: A non-refundable fee payable to NRB upon submission of the application.

- Minimum capital requirement: This is the most substantial cost. The amount varies depending on the type of bank, but it can range from NPR 2 billion for development banks to NPR 8 billion for commercial banks.

- Legal and consulting fees: Engaging lawyers, financial advisors, and other consultants to assist with the application process.

- Document preparation costs: Expenses related to preparing the business plan, financial projections, and other required documents.

- Infrastructure setup: Costs associated with establishing physical branches, IT systems, and other necessary infrastructure.

- Staffing costs: Expenses related to hiring and training key personnel.

- Compliance costs: Ongoing expenses to ensure adherence to regulatory requirements.

It’s important to note that these costs can add up to a significant amount. Prospective bank owners should have a clear financial plan to cover not just the licensing costs, but also the operational expenses until the bank becomes profitable.

While the costs are substantial, they serve as a barrier to entry that helps ensure only serious and well-prepared entities enter the banking sector, contributing to the overall stability of Nepal’s financial system.

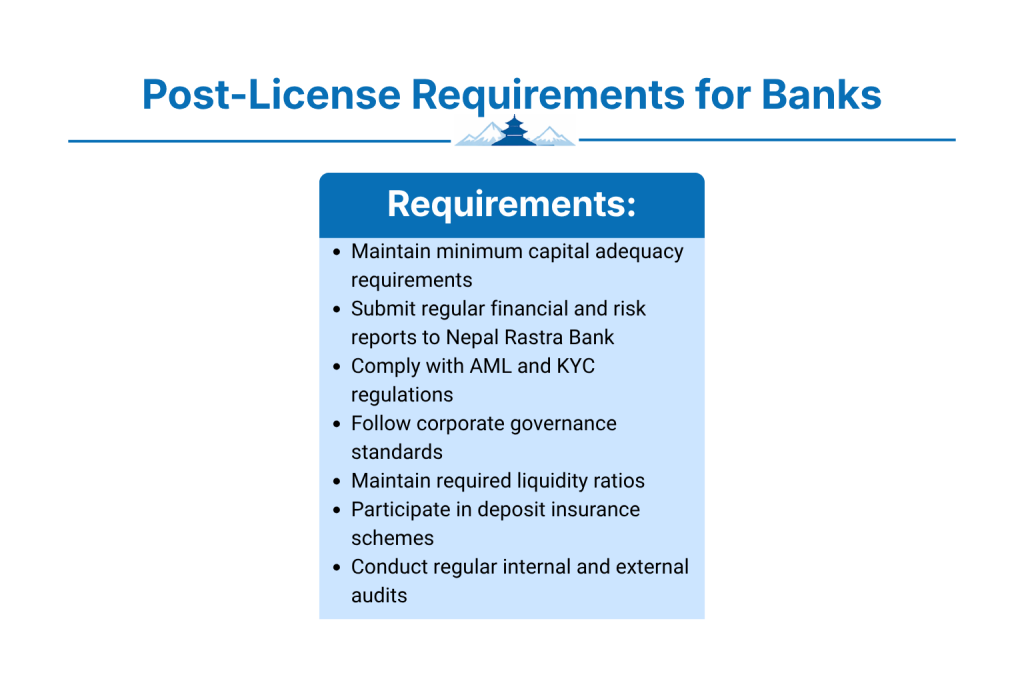

What are Post-License Requirements for Banks?

Obtaining a banking license is just the beginning. Once licensed, banks in Nepal must adhere to various ongoing requirements to maintain their license and operate legally. Some key post-license requirements include:

- Maintaining minimum capital adequacy ratios

- Regular reporting to NRB on financial performance and risk metrics

- Compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations

- Adhering to corporate governance standards

- Maintaining required liquidity ratios

- Participating in deposit insurance schemes

- Regular internal and external audits

These requirements are designed to ensure the ongoing stability and integrity of the banking system. NRB conducts regular inspections and may require corrective actions if a bank falls short of these standards.

Banks must also stay updated on changing regulations and adapt their operations accordingly. This often requires ongoing investment in compliance systems and staff training.

Failure to meet these post-license requirements can result in penalties, restrictions on banking activities, or in severe cases, the revocation of the banking license. Therefore, it’s crucial for banks to view compliance as an ongoing commitment rather than a one-time hurdle during the licensing process.

What Types of Banking Licenses are Available?

Nepal’s banking sector offers several types of licenses, each catering to different financial services and market segments. The main types of banking licenses available in Nepal are:

- Commercial Banks (Class A): These are full-service banks that can offer a wide range of banking services, including accepting deposits, providing loans, and dealing in foreign exchange.

- Development Banks (Class B): These banks focus on promoting economic development, often specializing in specific sectors or regions.

- Finance Companies (Class C): These institutions typically offer more limited services compared to commercial banks, often focusing on consumer finance and leasing.

- Micro-Finance Institutions (Class D): These organizations specialize in providing small loans and financial services to underserved populations, particularly in rural areas.

Each type of license comes with its own set of requirements, particularly in terms of minimum capital and permitted activities. The choice of license depends on the applicant’s business model, target market, and financial capacity.

It’s worth noting that NRB periodically reviews and may revise the classification and requirements for different types of financial institutions. Always check the latest regulations when considering which type of license to pursue.

What are the Benefits of Having a Banking License?

Obtaining a banking license in Nepal offers numerous benefits, making it an attractive prospect for entrepreneurs and financial institutions:

- Legal operation: The license allows you to legally conduct banking activities in Nepal, protecting you from regulatory issues.

- Customer trust: A licensed bank inspires confidence among depositors and borrowers, facilitating business growth.

- Access to central bank facilities: Licensed banks can access various NRB facilities, including the lender of last resort function.

- Participation in the financial system: Licensed banks can engage in interbank lending and participate in the national payment system.

- Expansion opportunities: The license provides a platform for future growth and diversification of financial services.

- Contribution to economic development: Banks play a crucial role in Nepal’s economic growth by mobilizing savings and providing credit.

- Potential for profitability: Despite regulatory requirements, the banking sector in Nepal offers significant profit potential.

While the licensing process is rigorous, these benefits make it a worthwhile endeavor for those committed to entering Nepal’s banking sector. A banking license opens doors to numerous opportunities in one of South Asia’s growing economies.

In conclusion, obtaining a banking license in Nepal is a complex but rewarding process. It requires careful planning, significant investment, and ongoing commitment to regulatory compliance. However, for those willing to navigate this process, it offers the opportunity to play a vital role in Nepal’s financial sector and contribute to the country’s economic development.